Carl Levin, who is the inspiration for the Levin Center for Oversight and Democracy, represented Michigan as a Democrat in the U.S. Senate from 1979 to 2015. During his 36-year tenure, he chaired the Subcommittee on Oversight of Government Management, the Permanent Subcommittee on Investigations, and the Committee on Armed Services, becoming a leader and champion of fact-based, bipartisan, high-quality oversight investigations by Congress. He used his committee positions to investigate a wide range of issues including government mismanagement, money laundering, offshore tax abuse, corporate misconduct, ethics, torture, and more, producing not only blockbuster hearings and reports but also new laws to address identified problems.

Early Career

Sen. Levin was born and raised in Detroit, Michigan. He began his long career in public service at the Michigan Civil Rights Commission in 1964, where he worked as General Counsel until 1967.[1] He then headed the appellate division of Detroit’s Legal Aid Office until elected to the Detroit City Council in 1969. He served two terms, including in his second term as City Council President.

During his time on the City Council, Mr. Levin battled with the U.S. Department of Housing and Development (HUD) over failing federal housing programs that were devastating Detroit. Inflated mortgages from the Federal Housing Administration that homeowners were unable to pay led to abandoned houses that HUD then sold with multiple building code violations to unsuspecting new owners who also abandoned them because they did not have the ability to pay for necessary repairs. The number of blighted and abandoned houses in Detroit increased dramatically. The city wanted to tear them down as a danger to the community, but because they were government-owned, they couldn’t, and HUD refused to take action. After repeated attempts to negotiate a solution, the City Council secured a legal opinion from the City Corporation Counsel determining that the city had the right to demolish abandoned buildings as part of the city’s duty to protect its citizens.[2] Despite threats from HUD that he would be arrested and prosecuted, Mr. Levin personally directed the first bulldozer that knocked down a dilapidated, vacant house.

That experience had a lasting effect on Sen. Levin and influenced his philosophy of public service for the rest of his life. He explained in his autobiography:

Holding government accountable and ensuring that legislatively authorized programs are run effectively and efficiently were major guideposts during my service on the Detroit City Council, during my first campaign, and throughout my Senate career. As a former local official, I understand the importance of responding to people in need, listening to even the smallest voice, and working hard on behalf of the people with honesty, integrity, and civility.[3]

Subcommittee on Oversight of Government Management

In 1979, after a spirited campaign launched him from the City Council to the U.S. Senate, Sen. Levin joined the committees on Armed Services, Governmental Affairs, and Small Business. Upon learning of his interest in government oversight, Sen. Abraham Ribicoff of Connecticut, Governmental Affairs Committee chair, created the Subcommittee on Oversight of Government Management (OGM) especially for Sen. Levin and appointed him the subcommittee chair. Sen. Levin helped lead the subcommittee for over a decade, taking on multiple issues while honing his skills as an investigator. During that time he also developed a close working relationship with his Republican counterpart, Sen. William Cohen from Maine. The senators traded places over the years as subcommittee chair and ranking member as majority control of the Senate shifted between the two major political parties.

Sen. Levin led multiple OGM investigations into a wide range of complex oversight issues, including massive backlogs and denials of applications for social security disability benefits, kickbacks paid to Department of Defense (DOD) contract officers to obtain contract work, lax enforcement of antidumping duties intended to combat unfair trade, weak debarment rules that allowed contractors debarred by one federal agency to bid on contracts with other federal agencies, safety problems with contractors working on chemical and biological warfare matters, and poor management of Great Lakes oil spills.

Perhaps the most famous OGM investigation led by Sen. Levin examined wrongdoing by Wedtech, a company that pulled strings in the White House to win multi-million-dollar DOD contracts it lacked the expertise to perform. Wedtech also managed to keep its designation as a small business long after the Small Business Administration should have ended it. To piece together what happened, the subcommittee conducted over 150 interviews, compiled and reviewed over 30 boxes of documents, and won a battle to obtain White House records.

In 1987, as part of a series of hearings, the subcommittee called as a witness then Attorney General Edwin Meese who had helped Wedtech while he was a senior White House counsel – the only time he appeared as Attorney General before a congressional subcommittee. Among other issues, Sen. Levin pressed him on why he’d failed to include on his financial disclosure statement profitable investments that had been arranged for him by Wedtech consultant Franklyn Chinn.

In 1988, PSI issued a bipartisan report on Wedtech, supported by Sen. Cohen and other subcommittee Republicans, describing evidence of improper corporate influence, contract mismanagement, and questionable decision-making by several federal agencies as well as unethical conduct by multiple federal employees. The report found, in particular, that Mr. Meese had violated a White House policy against contacting procurement officials about a specific contract and had failed to disclose investments arranged by Mr. Chinn.

The report triggered an independent counsel investigation into Mr. Meese’s conduct. The independent counsel concluded that Mr. Meese had “probably violated” a federal conflict of interest law in connection with Wedtech and failed to disclose certain income on his federal tax return, but did not charge him with a crime. Claiming vindication, Mr. Meese nevertheless resigned his post as Attorney General, a step that Sen. Levin had earlier advocated.

Over time, more than a dozen federal, state, and local officials were convicted of bribery and other offenses involving Wedtech. In the meantime, Sens. Levin and Cohen developed legislation to strengthen federal disclosure requirements for lobbyists who contact senior agency officials or members of Congress. After years of effort, the Levin-Cohen Lobbying Disclosure Act was enacted into law in 1995.

In addition to his OGM work, Sen. Levin took an active role in many oversight investigations conducted by the full Committee on Governmental Affairs, again often in coordination with Sen. Cohen. One example is a full committee investigation of troubling procurement practices at DOD. Sens. Levin and Cohen took the lead in exposing how two-thirds of DOD contracts were issued without competitive bids and how the lack of competition led to inflated prices, including the purchase of $640 toilet seats.[4] The two senators subsequently introduced the Cohen-Levin Competition in Contracting Act to require federal agencies to make greater use of full and open competitive bidding procedures. An amended version of their bill was enacted into law as part of the Deficit Reduction Act of 1984, and has since become one of the foundations of federal contracting.

Permanent Subcommittee on Investigations

“He has used PSI in the way it was intended by Harry Truman.”

Sen. Al Franken

In 1999, Sen. Levin became the senior Democrat on the Permanent Subcommittee on Investigations (PSI), the Governmental Affairs Committee’s most powerful and respected investigative subcommittee. He spent the rest of his Senate career in leadership positions on PSI, serving either as its ranking minority member or chair.

He began his PSI tenure when Sen. Susan Collins of Maine was the subcommittee chair. In 2001, the Senate switched to Democratic control, and he took the helm from Sen. Collins, chairing PSI from 2001 to 2002. In 2003, the Senate reverted to Republican control, and Sen. Levin returned to ranking member while Sen. Norm Coleman of Minnesota served as PSI chair from 2003 to 2007. At that point, the Senate shifted control once more, and Sen. Levin again served as PSI chair from 2007 until his retirement in January 2015. During those latter years, Sen. Tom Coburn of Oklahoma and Sen. John McCain of Arizona served, in turn, as PSI’s ranking Republican. During the course of his 15 years in PSI leadership, Sen. Levin worked closely with each of his four Republican partners, ensuring all PSI investigations proceeded on a bipartisan basis.

Sen. Levin used his PSI investigative authority primarily to examine complex financial matters including financial engineering, abusive tax shelters, and Wall Street wrongdoing. Three high-profile inquiries garnered especially intense media attention.

- In 2001, Enron, the seventh largest U.S. corporation, suddenly declared bankruptcy, upending investors, employees, and creditors across the country and sparking multiple congressional investigations, including a year-long PSI inquiry. To untangle Enron’s financial maneuvering, PSI issued more than 75 subpoenas, gathered nearly two million pages of documents, conducted 100 interviews, issued three bipartisan reports, and held four days of hearings. The Levin-Collins hearings and reports provided dramatic and detailed information about Enron’s skullduggery and helped enact the 2002 Sarbanes-Oxley Act strengthening safeguards against corporate financial deceptions and complicit accounting firms. More information can be found in the Levin Center portrait, “Congress and the Enron Scandal,” that details multiple congressional investigations into the Enron disaster.

- In 2003, PSI held hearings and issued a report on how U.S. accounting firms – KPMG, in particular – were designing and mass marketing abusive tax shelters to help wealthy individuals and profitable corporations cheat on their taxes. A KPMG whistleblower kindled the investigation by supplying PSI with a roster of KPMG tax shelter products and clients. PSI also subpoenaed KPMG documents which the firm’s tax leadership secretly resisted until the firm as a whole found out and immediately provided the requested documents. PSI hearings disclosed that KPMG had created an internal “Tax Innovation Center,” developed over 500 tax shelters, wrote legal opinions claiming they complied with the tax code even when internal experts disagreed, and mass marketed and executed numerous complex tax shelters in return for lucrative fees. In response, the IRS stepped up its enforcement activity and collected more than $3.7 billion in connection with one set of fraudulent tax shelters marketed by KPMG and Ernst &Young. In 2005, the IRS issued an award to PSI staff for assisting in that tax shelter investigation.[5]

- A two-year PSI investigation was sparked by the 2008 financial crisis which saw the U.S. mortgage market collapse, storied financial firms go under, and millions of Americans lose their jobs and homes. The inquiry culminated in four hearings in which PSI grilled executives from Goldman Sachs, Washington Mutual, Moody’s, Standard and Poor’s, and regulators from the Office of Thrift and Supervision about their roles in the financial meltdown. The Levin-Coburn hearings were followed by a 750-page, bipartisan report from the subcommittee, the only financial crisis investigation to produce bipartisan findings and recommendations. In addition, PSI’s final Goldman Sachs hearing generated such bipartisan outrage over Wall Street misconduct that the Senate ended a filibuster the next day, leading to passage of the Dodd-Frank Reform and Consumer Protection Act. More information about that PSI financial crisis investigation can be found in the Levin Center portrait of Sen. Coburn.

Sen. Levin became known for his ability to tackle Wall Street misdeeds, explain the intricacies of complex wrongdoing, and recommend reforms. Other examples include Levin-led PSI inquiries into the so-called London whale scandal involving billions of dollars in credit derivative trading losses; suspect bank activities involving physical commodities like oil, aluminum, jet fuel, and copper; natural gas speculation by a small hedge fund that fueled multi-billion-dollar price manipulation and volatility; bank schemes enabling hedge funds to dodge paying taxes on stock dividends; and high frequency trading problems in U.S. stock markets. He also investigated financial firms that designed and executed complex offshore tax shelters for wealthy corporate executives like Sam and Charles Wyly and Robert Wood Johnson.

In addition to investigating financial scandals, Sen. Levin used PSI to expose corporate abuses that directly harmed average Americans, including unfair credit card practices, deceptive sweepstakes contests, and excessive gasoline prices.

- In 2007, Sen. Levin opened an investigation into U.S. credit card abuses affecting hundreds of millions of U.S. households. At hearings in March and December, witnesses testified about interest charges on credit card debt already paid, multiple late fees for a single late payment, and retroactive interest hikes imposed on cardholders who had met their commitments and never missed a payment. A dramatic example was Wesley Wannemacher who used a new credit card to pay for wedding expenses and charged $3,200, which was $200 over his limit. Six years later when he appeared before the subcommittee, he had paid $6,300 on the debt but still owed $4,400. Chase had charged him $1,500 in over-the-limit fees, $1,100 in late fees despite on-time payments, and $4,900 in penalty interest charges. Chase, Bank of America, and Citicard executives also testified at the hearing, and announced changes to dubious practices. Sen. Levin and Sen. Claire McCaskill from Missouri worked with Sen. Christopher Dodd of Connecticut from the Senate Banking Committee on legislation mandating an array of credit card reforms. Congress enacted the related bipartisan Credit Card Accountability, Responsibility, and Disclosure Act on May 22, 2009. One study calculated that from 2011 to 2014, the law saved consumers $16 billion.

- In his first year on PSI as ranking Democrat, Sen. Levin worked with PSI Chair Collins to hold hearings in March and July 1999, on deceptive sweepstakes contests that flooded American households with 100 million mailings per year. Elderly witnesses and their children testified that misleading mailings encouraged recipients to spend substantial sums on sweepstakes they were unlikely to win. Deceptive language included statements that implied winning was guaranteed upon entering a contest or became more likely with repeated purchases from the sweepstakes company. Some mail used small type the elderly had difficulty reading or falsely indicated the mailing was approved by the government. Some sweepstakes companies made it nearly impossible to remove names from their mailing lists. Some sweepstakes led seniors to impoverish themselves. In response, on December 12, 1999, Congress enacted the Deceptive Mail Prevention and Enforcement Act, which had been introduced by Sen. Collins and cosponsored by Sen. Levin. The new law required sweepstakes mailings to state clearly that no purchase was necessary to win and specify the odds of winning. It also authorized the U.S. Postal Service to stop delivery of deceptive mail and penalize responsible companies. It required the sweepstakes industry to remove persons from their mailing lists upon request.

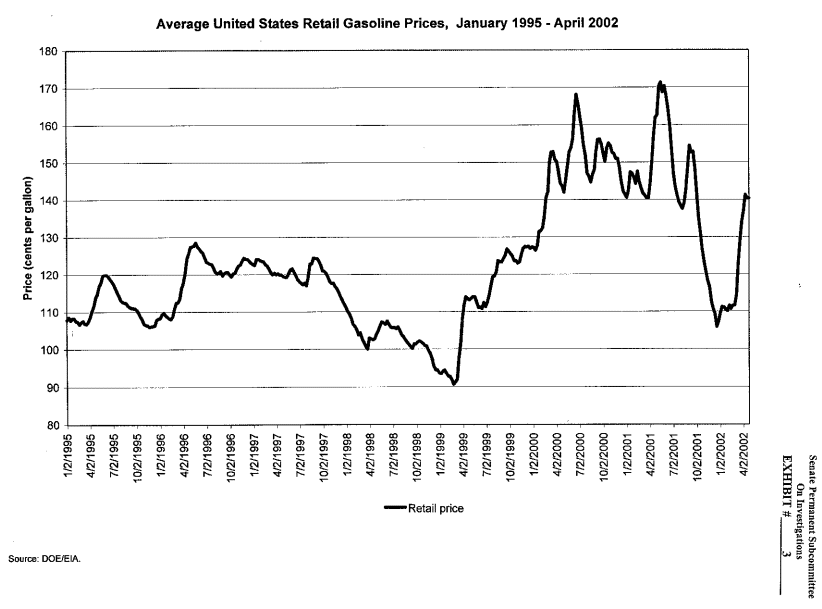

- Spiking gasoline prices in Michigan spurred another Levin-led PSI investigation in 2001. After a year-long inquiry gathered over 103 boxes of documents and other evidence, PSI held hearings and released a 400-page staff report exposing improper actions taken by some oil companies to hike prices by reducing gasoline supplies. Suspect actions included limiting gasoline production and importation, blocking new refineries, changing gasoline specifications, and exporting gasoline out of certain regions. A memo uncovered from Marathon oil company even praised Hurricane Georges, because it had “caused some major refinery closures, threatened offshore oil production and imports, and generally lent some bullishness to the oil futures market.”[6] The report also determined that oil companies had gained an additional $1 billion in income annually for every one-cent per gallon increase in gasoline prices. At the 2002 hearings, Sen. Levin grilled executives from ExxonMobil, Marathon, BP, ChevronTexaco, and Shell Oil.

- Sen. Levin also directed his subcommittee staff to investigate and issue a follow-up report examining how changes in crude oil prices impacted gasoline prices. The report found, in part, that a 2002 Department of Energy effort to increase oil stored in the U.S. Strategic Petroleum Reserve (SPR) had removed 40 million barrels of high-priced crude oil from the marketplace and, by reducing supplies, increased crude oil prices. Those price hikes, in turn, boosted the price of oil-based products, including hiking “home heating oil by 13%, jet fuel by 10%, and diesel fuel by 8%, imposing on U.S. consumers additional total fuel costs of between $500 million and $1 billion.”[7] A 2003 Levin-Collins amendment to block SPR purchases until crude oil prices fell below a specified level passed the Senate but did not become law. Five years later, in 2008, Congress enacted the Levin-Collins approach in the Strategic Petroleum Reserve Fill Suspension and Consumer Protection Act.

Money Laundering Through U.S. Banks

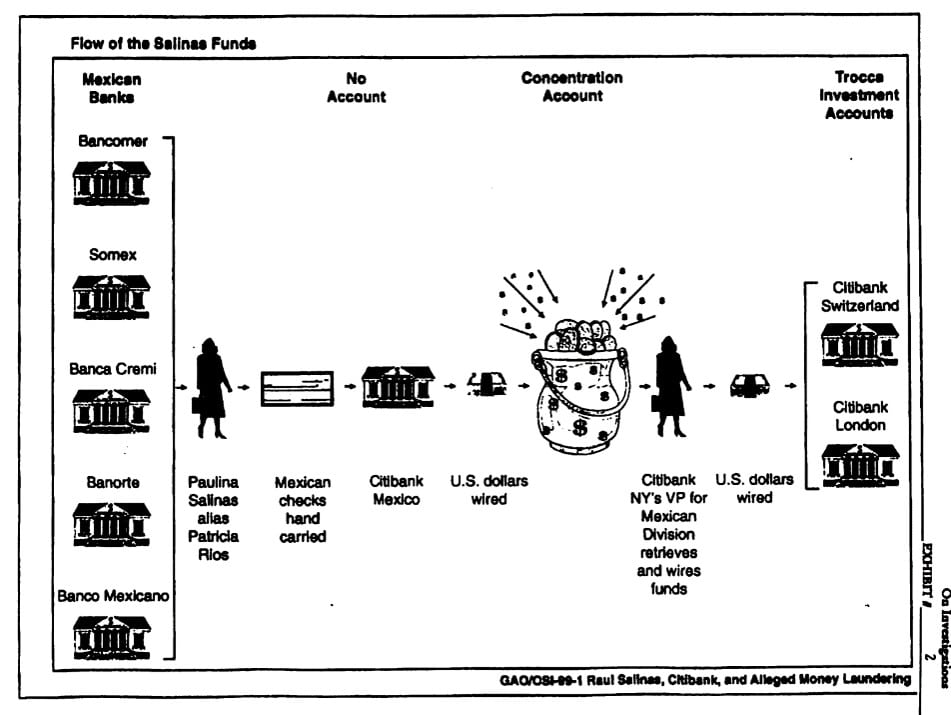

One of the most famous and influential series of PSI hearings led by Sen. Levin involved money laundering through U.S. banks. It began with the very first Levin-led PSI investigation which focused on money laundering through Citigroup, a leading U.S. financial institution. The inquiry was triggered by a worldwide scandal involving Raul Salinas, brother of the then President of Mexico, Carlos Salinas. In 1998, Raul Salinas was arrested in Mexico on suspicion of murdering his former brother-in-law, a prominent politician, after which his wife was caught attempting to withdraw over $84 million from a Swiss bank. A Swiss court later found that Raul Salinas had used multiple Swiss accounts to launder over $100 million related to drug trafficking.

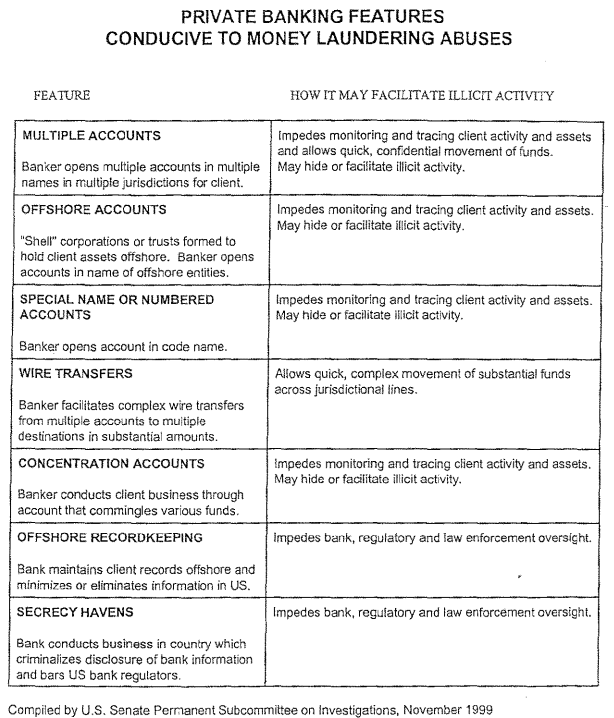

Media reports also disclosed that Raul Salinas had large accounts at Citigroup, including Citigroup’s “private bank” – a bank division catering to wealthy clients making a minimum deposit of at least $1 million. Private bank clients are routinely assigned a private banker and offered an array of services which at the time included servicing offshore entities and accounts. PSI learned that the Federal Reserve had conducted three audits of Citigroup private bank’s anti-money laundering controls in 1996, 1997, and 1998, identified numerous deficiencies, and noted that at the private bank, “the corporate culture . . . does not foster a ‘climate of integrity, ethical conduct and prudent risk taking’ by U.S. standards.”[8] To learn more, PSI reviewed the Federal Reserve audit records for the private bank.

The Federal Reserve records led PSI investigators to examine not only transactions involving the Salinas accounts but also private banking accounts opened for Omar Bongo, then-president of Gabon; Asif Ali Zardari, husband of Pakistan’s former Prime Minister Benazir Bhutto; and Mohammed, Ibrahim, and Abba Abacha, sons of then Nigerian president Sani Abacha. PSI learned that the private bank had knowingly helped each of them form offshore shell entities, open secret offshore accounts, and move millions of dollars in suspect funds across international lines despite signs of corruption or other wrongdoing.

To assist the inquiry, PSI asked the Government Accountability Office (GAO) to determine how Citigroup had helped Raul Salinas move over $90 million from Mexico to private bank accounts in London and Switzerland. GAO reported, and PSI confirmed, that Citibank’s Mexican branch had knowingly accepted bank checks hand delivered by Mr. Salinas’ then girlfriend (later wife), deposited those checks into the private bank’s own internal account without indicating who owned the funds, transferred the money to Citibank headquarters in New York, and then moved the still-undesignated funds into shell company and other disguised accounts at the private bank’s branches in London and Switzerland.

PSI demonstrated that Citigroup’s private bank also knowingly moved millions of dollars in suspect funds for the Bongo, Zardari, and Abacha accounts. To follow the money, PSI subpoenaed documents and conducted almost 100 interviews. In November 1999, PSI released a 65-page Levin staff report and held two days of hearings presenting the evidence it had collected. The hearings were chaired by Sen. Collins who had worked closely with Sen. Levin to expose Citigroup’s misconduct.

The 1999 hearings garnered worldwide attention. They became the first in a long series of Levin-led PSI hearings and reports examining money laundering vulnerabilities and deficiencies at U.S. financial institutions. Subsequent hearings focused, for example, on U.S. banks administering accounts for suspect foreign banks, suspicious Riggs Bank accounts opened for foreign officials, shell company and law firm accounts opened by U.S. attorneys for foreign dictators and their family members, and U.S. accounts opened by HSBC for money launderers, drug traffickers, and other wrongdoers. To address the identified anti-money laundering deficiencies, Sen. Levin was able to win enactment of new laws to strengthen U.S. safeguards against money laundering and corruption.[9]

Tax Haven Banks

Sen. Levin didn’t stop there. He also exposed how non-U.S. banks located in tax havens were deliberately helping U.S. clients open secret offshore accounts, form offshore entities, and hide assets from the U.S. Internal Revenue Service (IRS) to evade U.S. taxes. This PSI inquiry was triggered by two separate incidents in 2007, in which confidential sources knocked on PSI’s doors and alerted PSI investigators to hidden misconduct. It led to several PSI hearings with worldwide impact.

The first confidential informant was a computer specialist who’d been hired by LGT Bank & Trust Company in Liechtenstein to create a paperless office. He gave PSI 12,000 pages of LGT records showing that the bank had opened secret accounts for over 150 wealthy Americans. The records showed that LGT had knowingly taken steps to conceal its U.S. client accounts by, among other actions, failing to disclose them in required reports to the IRS, opening the accounts in the names of offshore entities controlled by the U.S. clients, withholding mail that would otherwise have been sent to U.S. addresses, calling the U.S. clients from pay telephones to disguise calls from the bank, and using code names in place of client names. Accounts were often opened using a legal entity specific to Liechtenstein, known as a “foundation,” using documents that included secrecy provisions to prevent the disclosure of financial information to third parties, including governments. The biggest LGT account disclosed by PSI held $68 million.[10]

The second confidential informant was a former private banker from UBS, the largest bank in Switzerland. He disclosed to PSI that UBS routinely sent private bankers to the United States to service existing clients and find new ones, often visiting events that attracted wealthy individuals such as yacht races and art shows. To confirm the information, PSI obtained U.S. customs records showing that 20 “client advisors” from UBS had traveled from Switzerland to the United States more than 300 times between 2001 and 2008.[11] A later hearing disclosed evidence that UBS private bankers had, in fact, traveled to the United States about 3,800 times in a single year to visit and recruit clients. In addition, the hearing highlighted an internal 2004 bank report stating that UBS held nearly $18 billion in Swiss accounts for approximately 52,000 “account relationships” with U.S. clients who had not declared those accounts to the IRS.

In July 2007, PSI released a 130-page, bipartisan Levin-Coleman report detailing how wealthy Americans had hidden assets in the Liechtenstein and Swiss banks, and estimated that Americans with hidden offshore accounts resulted in an overall loss of $100 billion in tax revenues every year. PSI also held two days of hearings to present the evidence to the public. LGT declined an invitation to the hearings, but video testimony from the LGT whistleblower, who had by then entered a witness protection program, described how he had found “evidence of LGT’s helping corrupt government officials, criminals, and tax evaders hide and transfer funds.”[12] U.S. citizens with LGT accounts were also called to testify but asserted their Fifth Amendment rights against self-incrimination and declined to answer the subcommittee’s questions.

UBS sent Mark Branson, chief financial officer of its Global Wealth Management and Swiss Businesses, to appear at the hearing. He provided the hearing’s most unexpected and stunning testimony when he apologized for the bank’s misconduct and promised it would no longer open secret accounts for U.S. clients:

“I am here to make absolutely clear that UBS genuinely regrets any compliance failures that may have occurred. We will take responsibility for them. We will not seek to minimize them. On behalf of UBS, I am apologizing. … We have decided to exit entirely the business in question. That means UBS will no longer provide offshore banking or securities services to U.S. residents through our bank branches. … We are working with the U.S. Government to identify those names of U.S. clients who may have engaged in tax fraud.”[13]

Later, in a February 2009 deferred prosecution agreement with the Department of Justice (DOJ), UBS admitted to participating in a criminal conspiracy to defraud the United States of tax revenue. UBS also agreed to pay a criminal fine of $780 million, inform the IRS of any new Swiss accounts opened by U.S. taxpayers, and turn over the names of certain U.S. clients with undeclared accounts. The UBS admission of guilt was a bombshell in the offshore world, marking the first break in what had been, until then, an impenetrable wall of Swiss secrecy in offshore banking.[14]

In March 2009, the IRS established the Offshore Voluntary Disclosure Program to encourage taxpayers to disclose any offshore accounts, assets, or income in exchange for reduced penalties. Over 100,000 taxpayers eventually took advantage of that and other IRS voluntary programs to disclose secret offshore accounts and pay back taxes, interest, and penalties exceeding $11 billion.

In 2010, partly in response to the PSI hearings, Congress enacted the Foreign Account Tax Compliance Act (FATCA) authored by Rep. Charlie Rangel of New York and Sen. Max Baucus of Montana. FATCA requires foreign financial institutions to disclose to the IRS all accounts opened by U.S. persons or pay a 30% tax on their U.S. earnings.[15] Since almost all foreign financial institutions hold U.S. treasuries, stocks, or bonds and earn U.S. income, almost all were subject to the FATCA tax and decided to comply with the new disclosure mandate. Over the next six years, the United States entered into arrangements and agreements with 113 countries, including Switzerland and Liechtenstein, to facilitate FATCA disclosures by more than 400,000 foreign financial institutions that have now registered with the IRS.

In the middle of U.S. efforts to implement FATCA, Sen. Levin and his PSI staff learned that Credit Suisse, the second largest bank in Switzerland, had failed to close thousands of secret Swiss accounts opened for U.S. clients, despite promising to close them after the UBS hearing in 2008. Further investigation determined that, at its peak, Credit Suisse had opened nearly 22,000 Swiss accounts for U.S. clients with about $10 billion in hidden assets. The bank had also used many of the same secrecy tricks as other tax haven banks: opening accounts in the names of offshore entities, quietly flying bankers into the United States to service and recruit new clients, and failing to disclose the Swiss accounts to the IRS in required reports. Credit Suisse even opened a branch in the Zurich airport so foreign account holders could fly in, do their banking, and fly out. Approximately 10,000 of its U.S. client accounts were managed there.[16]

PSI further learned that DOJ, under President Barack Obama, had largely stopped prosecuting U.S. taxpayers with undeclared Swiss accounts. U.S. prosecutors were relying on requests for information made through the U.S.-Swiss tax treaty rather than using U.S. courts to obtain information as DOJ had with UBS. The result was that DOJ had obtained the names of only 238 of the 22,000 Credit Suisse accountholders.

In February 2014, Sens. Levin and McCain held a hearing and issued a joint 200-page report focused on Credit Suisse’s misconduct. Credit Suisse officials attempted to blame a “small group” of bankers and employees for its misdeeds, while promising again to close the secret accounts. For their part, DOJ officials claimed the department was effectively enforcing the laws despite the paucity of legal action against U.S. taxpayers hiding funds at Credit Suisse. Three months after the hearing, Credit Suisse pled guilty to aiding and abetting U.S. tax evasion and paid a criminal fine of $2.6 billion.

Sen. Levin’s tax haven bank battle spanned a period of five years, with the 2008 UBS and 2014 Credit Suisse hearings serving as bookends. In 2016, the first FATCA disclosures of foreign accounts opened by U.S. persons began to be filed with the IRS. By then, a FATCA-style global disclosure regime known as the Common Reporting Standards also took effect enabling tax authorities in over 100 countries to exchange automated information about foreign accounts opened by their nationals. The resulting worldwide disclosure system not only made evading taxes by hiding assets in offshore accounts a lot harder, but also demonstrated how congressional oversight hearings could have a global impact.

Corporate Tax Dodging

An account of Sen. Levin’s PSI investigative work would not be complete without chronicling some of his efforts to combat corporate tax dodging. In those PSI hearings, executives from some of America’s largest multinational corporations were the recipients of his bespectacled gaze and intense questioning about why their tax payments were so low compared to their profits. Four examples illustrate Sen. Levin’s tenacity, analysis, and skill in exposing dubious corporate tax practices.

- Microsoft. In 2012, PSI held a hearing exposing how Microsoft, an iconic American corporation, took advantage of America’s workforce, ingenuity, and strong court system to develop, sell, and protect its patented products but then transferred the “economic rights” to market those patented products to its subsidiaries in Puerto Rico, Ireland, and Singapore. Afterwards, Microsoft paid licensing fees to its own subsidiaries, thereby drastically reducing its reported U.S. profits and related U.S. tax liability. A former PSI staff director explained:

“Under the intra-company agreements, from 2009 to 2011, Microsoft USA paid fees totaling nearly $21 billion, or almost half of its U.S. retail sales net revenue, to Microsoft Puerto Rico. Microsoft sent those billions of dollars … to Puerto Rico even though its products were developed, marketed, and sold to customers right here in the United States. By sending its U.S. funds offshore, Microsoft avoided paying any U.S. tax on nearly half its sales income.”[17]

In the three years PSI examined, it calculated that Microsoft had dodged U.S. taxes totaling $4.5 billion each year and negotiated a tax rate with Puerto Rico of less than 2%. Microsoft USA set up similar arrangements with Microsoft Ireland and Microsoft Singapore, using tax loopholes known as the “check-the-box” rule and the “CFC Look-Through” law to avoid paying U.S. taxes on its “offshore” profits, even though most of those profits were deposited into U.S. financial institutions.[18] In 2012, the IRS commenced an audit of Microsoft’s offshore tax practices; Microsoft has since opposed the IRS’ information requests in a years-long, ongoing court battle to avoid paying additional U.S. tax.

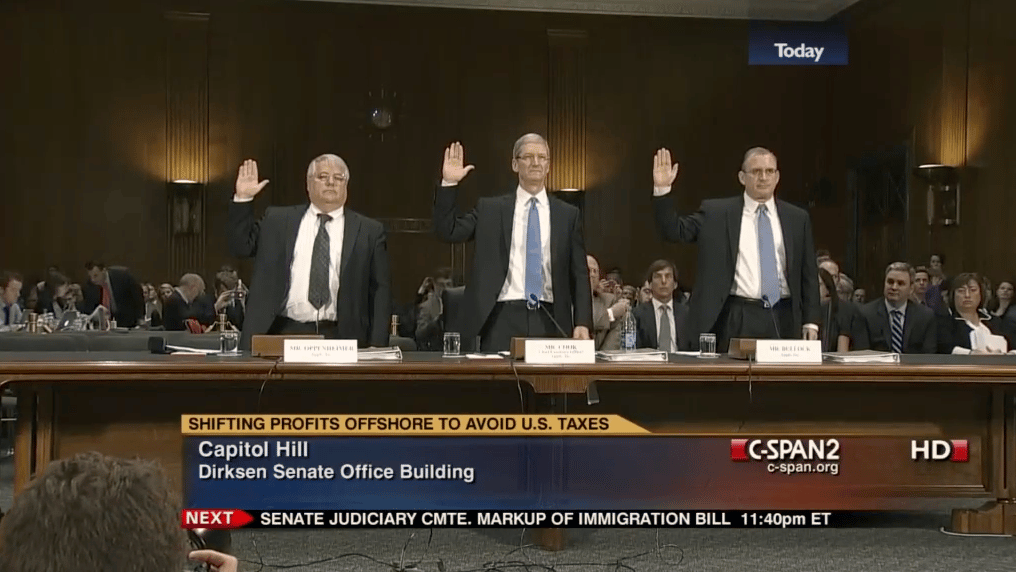

- Apple. In 2013, PSI turned the tax spotlight on Apple, another iconic American corporation and one of the most profitable in the world. In his opening statement at the hearing, Sen. Levin explained how Apple had created three new offshore subsidiaries, decided they were not tax residents of any country, and directed tens of billions of dollars in profits to them without paying U.S. taxes:

“Apple has sought the Holy Grail of tax avoidance …. Apple Inc. has created three offshore corporations, entities that receive tens of billions of dollars in income, but which have no tax residence – not in Ireland, where they are incorporated, and not in the United States, where the Apple executives who run them are located. Apple has arranged matters so it can claim that these ghost companies, for tax purposes, exist nowhere.”[19]

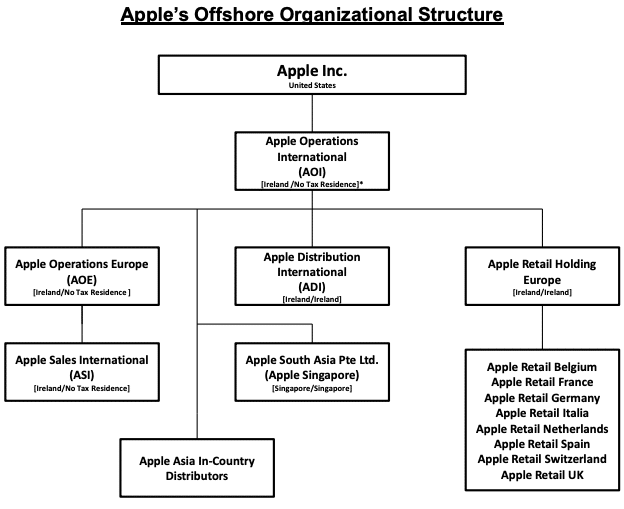

Apple’s new offshore subsidiaries, Apple Operations International (AOI), Apple Operations Europe (AOE), and Apple Sales International (ASI), were all incorporated in Ireland, but had no physical offices or employees there. Instead, all three shell entities were then managed by Apple employees located in the United States. Because Irish law taxed corporations “managed” in Ireland and U.S. law taxed corporations incorporated in the United States, Apple claimed that its U.S.-managed, but Irish-incorporated subsidiaries fell through the cracks and were not tax residents of either country.

At the hearing, PSI disclosed that, over a three-year period from 2009 to 2011:

- Non-U.S. Apple subsidiaries transferred a total of $74 billion in profits to ASI through the payment of licensing fees required by Apple for them to sell patented Apple products; ASI then paid taxes on those profits at a rate of 2% or less due to a secret sweetheart deal it had negotiated with Ireland whose statutory tax rate was 12.5%.

- In 2011 alone, despite profits of $22 billion, ASI paid only $10 million in taxes to Ireland, a near-zero rate of 0.05%.

- During the same three-year period, ASI issued $30 billion in dividends to AOE which, in turn, forwarded the dividends to AOI which did not file any tax return or pay any tax to any country on those profits.

- The agreement establishing the licensing arrangements for ASI was signed by top Apple executives in California including Tim Cook, who later became Apple’s CEO.

One of the tax experts at the hearing, Professor J. Richard Harvey of Villanova School of Law and Graduate Tax Program, noted that the offshore licensing arrangement used by Apple and other U.S. multinational corporations to evade U.S. tax “is largely unavailable to purely domestic businesses including almost all small business enterprises. Yet small businesses and individuals must make up the lost taxes.”[20] Mr. Cook countered that Apple had done nothing wrong: “We pay all the taxes we owe, every single dollar.… We do not depend on tax gimmicks.”[21]

- Caterpillar. In 2014, PSI held a hearing and released a Levin staff report focused on Caterpillar, an American manufacturer headquartered in Peoria, Illinois. Caterpillar sold construction equipment worldwide, including replacement parts which were the most profitable sector of its business. Both the equipment and the parts were produced primarily in the United States; Caterpillar’s warehouses, logistics, and executives were also U.S.-located. As a result, for decades, Caterpillar had reported 85% or more of the profits from its parts sold outside of the United States as U.S. income subject to U.S. tax.[22]

- In 1999, however, the company paid its auditor, PricewaterhouseCoopers (PwC), $55 million for a customized tax shelter. Pursuant to that tax shelter, Caterpillar gave its Swiss affiliate Caterpillar SARL (CSARL) licensing rights to sell its products abroad for a fee, without changing any of its operations. Caterpillar then declared 85% of its profits in Switzerland and only 15% in the United States. In Switzerland, CSARL paid a 4% special tax rate it had negotiated with the Swiss government. Caterpillar also boasted how it had dramatically lowered its U.S. taxes. PSI estimated that, from 2000 to 2012, Caterpillar transferred $8 billion in parts profits from the United States to Switzerland and avoided paying U.S. tax totaling $2.4 billion.

Sen. Levin released a 95-page majority staff report in connection with the hearing. Sen. McCain did not join the report, but his staff had fully participated in the Caterpillar investigation, and many of their comments were incorporated into the text. Sen. Levin’s PSI staff director at the time explained, “The doubts expressed by the McCain staff had energized us to be as thorough and persuasive as we could – which is exactly the way bipartisan oversight ought to work.”[23]

At the hearing, PwC accountants who developed the Swiss tax shelter claimed there was nothing untoward about selling Caterpillar the tax strategy and then having PwC auditors approve its use, even though the Sarbanes-Oxley Act enacted after the Enron collapse had established procedures to prevent the obvious conflict of interest. Caterpillar representatives testified that the IRS had essentially endorsed the corporation’s tax strategy by never objecting or proposing any tax adjustments. The corporation had made the same argument to the McCain staff to help persuade the senator not to join the Levin report.

After the hearing, however, PSI learned that three months prior to the April hearing, on December 23, 2013, the IRS had sent Caterpillar a notice which, in fact, objected to its “abusive corporate tax shelter” and stated the IRS would be seeking back taxes, interest, and penalties. The notice was accompanied by 70 pages of analysis supporting the IRS’s position.[24] Caterpillar has since admitted that the IRS is seeking to collect $2.3 billion related to the Swiss tax shelter but has rejected paying any tax. Also in 2013, the Public Company Accounting Oversight Board initiated a review of PwC’s conduct.[25] In 2020, the Senate Finance Committee raised questions about why, after seven years, the IRS collection effort against Caterpillar remains outstanding.

- Renaissance Technologies. A final example of Sen. Levin’s corporate tax work is a 2014 PSI hearing and report on a multi-billion-dollar tax dodge marketed by two large banks to a number of hedge funds, including Renaissance Technologies (RenTec). This PSI investigation dug into the details of the complex structured finance product sold by the banks. The banks claimed that using the structure could convert short term trading gains into long-term capital gains that benefited from a much lower tax rate. The scheme required the bank to set up a trading account, purchase a “basket” of securities through the account, and conduct securities trades while selling a hedge fund an “option” on the account proceeds that would mature in one year. The bank typically required the hedge fund to put up 10% of the cash needed to buy the securities and paid for the other 90%, ignoring a longstanding federal limit on bank lending for securities trading by clients.

- The structure created the appearance that the bank itself owned and traded the securities in the account, but evidence uncovered by PSI showed that, in fact, the hedge fund made all the trading decisions and reaped all the trading profits. In other words, the hedge fund was engaging in short term securities trades using bank-lent funds, not investing in a single, year-long option on an account under the bank’s control.

RenTec, the largest purchaser of the so-called basket options, used the accounts to conduct an estimated 100,000 trades each day or about 30 million trades a year. Its high-volume trading meant individual securities were held for weeks, days or even seconds. RenTec and the banks nevertheless claimed the fictional option structure collapsed those millions of individual trades into a single transaction, the execution of the option. They claimed the option structure magically transformed what would otherwise be short-term capital gains from an ordinary trading account into long-term capital gains subject to a lower tax rate. PSI staff estimated, based on the basket option profits reported by RenTec from 2000 to 2013, that RenTec had used the basket option structure to avoid paying U.S. taxes exceeding $6 billion.

The IRS had already initiated enforcement actions against basket option users, but the PSI hearing raised the visibility of the IRS efforts, produced new evidence of the scheme’s deceptive elements, and made it more difficult for RenTec and others to justify their actions. In 2021, seven years after the PSI hearing, RenTec paid the IRS $7 billion, one of the largest settlements in IRS history. A RenTec founder, James Simons, paid another $670 million to settle his personal tax liability from using basket options. Banks no longer sell the basket option structure.

These and other Levin-led PSI hearings drew U.S. and worldwide attention to the tax dodging practices of many multinational corporations, and other nations held their own hearings on the problem. The European Commission began to investigate and take action in some cases affecting the European Union, including ordering Ireland to collect back taxes from Apple totaling $14.5 billion, a decision which produced an international legal battle that remains ongoing. Additionally, in 2013, the OECD created the Base Erosion and Profit Shifting (BEPS) Project, a global collaboration to combat multinational corporation tax avoidance, finding that “(1) multinational corporations ought to pay taxes … and (2) corporate income taxes ought to be imposed where value is created.”[26] BEPS published an action plan to curb international corporate tax dodging, endorsed by more than 135 countries. One key recommendation was to require large multinational corporations to disclose to tax authorities their revenues and tax payments on an annual, country-by-country basis, a disclosure requirement put into effect by the United States in 2016.

When Sen. Levin retired in January 2015, the American Prospect wrote:

Levin elevated the public understanding of the calculated, deceptive strategies involved in the massive tax evasion among that thin but very rich slice of Americans who will commit felonies to escape taxes. Fair to say, Corporate America will not miss Levin, but honest taxpayers will.[27]

Similar tributes took note of his work on PSI to combat money laundering, Wall Street wrongdoing, and consumer abuses. The Levin-led PSI is even said to have inspired this New Yorker cartoon.

Armed Services Committee

At the same time Sen. Levin was conducting investigations at PSI, he was also leading important oversight inquiries during his years on the Senate Armed Services Committee (SASC), in particular while he chaired that committee from 2001 to 2003 and from 2007 to 2015. In addition to using routine SASC hearings to review a wide variety of DOD activities, Sen. Levin formed a committee investigative team to conduct specific inquiries.

The first inquiry undertaken by the SASC investigative team created by Sen. Levin examined the alleged torture and mistreatment of Al Qaeda and Taliban detainees in U.S. custody. Over the course of 18 months, the bipartisan SASC investigators collected and reviewed over 200,000 pages of classified and unclassified documents; interviewed over 70 individuals; and helped staff two SASC hearings in 2008. In November 2008, the committee unanimously approved a lengthy report which, after a DOD declassification process, was released to the public in April 2009. The bipartisan SASC report concluded in part:

The abuse of detainees at Abu Ghraib in late 2003 was not simply the result of a few soldiers acting on their own. Interrogation techniques such as stripping detainees of their clothes, placing them in stress positions, and using military working dogs to intimidate them appeared in Iraq only after they had been approved for use in Afghanistan and at GTMO. Secretary of Defense Donald Rumsfeld’s December 2,2002 authorization of aggressive interrogation techniques and subsequent interrogation policies and plans approved by senior military and civilian officials conveyed the message that physical pressures and degradation were appropriate treatment for detainees in U.S. military custody. What followed was an erosion in standards dictating that detainees be treated humanely.[28]

The SASC investigation took place prior to the longer inquiry undertaken by the Senate Select Committee on Intelligence whose more than 6,000-page report on the torture of detainees in U.S. custody has yet to be fully released to the public. Sen. Levin, in his role as SASC chair, automatically served as an ex officio member of the intelligence committee and contributed to its report. He spoke out publicly for both the preservation and public release of the entire intelligence committee report.

At Sen. Levin’s direction, the SASC investigative team also initiated an inquiry into DOD’s use of private security contractors in Afghanistan. The investigation, detailed in a 2010 report unanimously approved by SASC members, uncovered evidence of Afghan warlords and strongmen acting as force providers to security companies, contractors acting against U.S. and Afghan government interests, and dangerous gaps in U.S. military oversight. Ultimately, the committee determined that DOD reliance on private security contractors was inconsistent with its counterinsurgency strategy.

Another inquiry of note by the SASC investigative team under Sen. Levin was an examination of counterfeit electronic parts increasingly being found in U.S. military equipment, from aircraft to missiles to radios. This year-long bipartisan investigation culminated in a 2011 hearing and 2012 report which found not only “overwhelming evidence of large numbers of counterfeit parts making their way into critical defense systems,” but also that the parts could “compromise performance and reliability, risk national security, and endanger the safety of military personnel.” The investigation further determined that China was “the dominant source country” for the counterfeit parts.[29] In response to the problems uncovered by the investigation, the Senate enacted a Levin-McCain amendment designed to curb U.S. imports of counterfeit electronic parts and strengthen DOD and industry supply chain safeguards.[30]

Still another SASC inquiry by the Levin-led investigative team exposed previously unknown cyber intrusions into the computer networks of contractors working for the U.S. Transportation Command (TRANSCOM) which plays a central role in the mobilization, deployment, and sustainment of U.S. military forces. The 2014 SASC report revealed dozens of intrusions into TRANSCOM contractors in just a single year, nearly half of which were successful and many of which were attributed to China. The investigation also found serious weaknesses in TRANSCOM reporting requirements and gaps in DOD and law enforcement information sharing about cyber intrusions. The bipartisan report, unanimously adopted by voice vote, concluded that cyber intrusions by foreign countries, most of which TRANSCOM had been unaware of prior to the investigation, posed a threat to U.S. military operations.

Sen. Levin’s SASC oversight efforts extended far beyond the efforts of the investigative team and covered a broad range of topics — from DOD financial management issues to ammunition and readiness concerns, inadequate weapons testing, failure to utilize off-the-shelf purchasing, Strategic Defense Initiative cost overruns, nuclear proliferation problems, and decisions to attack Iraq and Afghanistan. In every case, Sen. Levin’s approach was to find out the facts first and work from there.

Sen. Levin’s commitment to bipartisan oversight and, as described by Sen. Dick Durbin of Illinois, “patient mastery of complex issues,”[31] was well-known and respected by his colleagues. At Sen. Levin’s Farewell to the Senate, Sen. McCain commended the PSI chair for “zealously and effectively pursuing his investigations in a way that has furthered the subcommittee’s long-standing tradition of bipartisanship. While Carl Levin and I may have had our disagreements, we never let them get in the way of finding common ground where we could.”[32] Sen. Collins recalled his hard work to find the truth:

He works well with Senators across the aisle because he works hard. From the very first time I saw Senator Levin in action back in 1978, I saw the importance he placed on extensive, exhaustive preparation for our committee investigations and hearings. As many evasive or ill-prepared witnesses learned to their chagrin, the eyes behind those trademark reading glasses focused like a laser because he has always done his homework.[33]

Post-Senate Years

Sen. Levin set a high standard for fact-based bipartisan oversight during his 36 years in the U.S. Senate. In retirement, he found another way to promote oversight by helping to establish the Levin Center for Oversight and Democracy at Wayne State University Law School in Detroit, Michigan, where he also taught. Sen. Levin fueled Center efforts to create bipartisan oversight training programs, strengthen oversight as an academic field of study, sponsor oversight conferences and events, and build a stronger oversight community. He also supported Center work to strengthen oversight efforts by the 50 state legislatures, in part because so many members of Congress began their careers as elected state legislators.

Sen. Levin continued to speak publicly about the importance of oversight, telling CQ Roll Call in 2017:

It is so important that the executive branch have a congressional branch which aggressively and effectively looks at programs to see whether or not the programs and the laws are working well, to see which new laws might be needed and to see what wrongdoings need to remedied.[34]

He also penned multiple articles on oversight issues, often reminding policymakers and the public: “Good government requires good oversight.”

Sen. Levin passed away in Detroit on July 29, 2021. Following his death, journalist Stephen Henderson eulogized him on his radio show:

Every memory I have of him is wrapped in this idea of statesmanship and grace. The idea of public service above everything else. He didn’t just talk about those things, he did them all the time. Never, never wavered. It’s not an understatement to say we just don’t have people like that in large number …. Carl Levin really did stand out, and in many ways, he stood alone.[35]

Learn More

- Levin’s farewell speech to the Senate

- Carl Levin: The Senator Who Mastered Oversight (Politico)

- The Legacy of Carl Levin (The American Prospect)

- Tributes in the Congress of the United States

- Getting to the Heart of the Matter, by Sen. Levin

- Financial Exposure: Carl Levin’s Senate Investigations into Finance & Tax Abuse, by Elise Bean

- Carl Levin Memorial Service

[1] Carl Levin: His life and career. (2014, September 7). Detroit Free Press. https://www.freep.com/story/news/local/2014/09/07/carl-levin-his-life-and-career-/15221117/

[2] Levin, C. M. (2021). Getting to the heart of the matter: My 36 years in the Senate [eBook edition]. Wayne State University Press.

[3] Levin, C. M. (2021).

[4] Levin, C. M. (2021).

[5] Bean, E. J. (2018).

[6] Gas prices: How are they really set?: Hearings before the Permanent Subcommittee on Investigations of the U.S. Senate Committee on Homeland Security and Governmental Affairs. 107th Cong. (2002). https://www.govinfo.gov/content/pkg/CHRG-107shrg80298/pdf/CHRG-107shrg80298.pdf

[7] Bean, E. J. (2018).

[8] Bean, E. J. (2018). Financial exposure: Carl Levin’s Senate investigations into finance and tax abuse. Palgrave Macmillan.

[9] See, e.g., Levin bill which was the basis for anti-money laundering provisions in Title III of the Patriot Act and a Levin-Coleman amendment which imposed a one-year cooling off period before federal bank examiners could take positions with the banks they examined, now codified at 12 U.S.C. 1820(k).

[10] Tax haven banks and U.S. tax compliance: Hearings before the Permanent Subcommittee on Investigations of the U.S. Senate Committee on Homeland Security and Governmental Affairs. 110th Cong. (2008). https://www.govinfo.gov/content/pkg/CHRG-110shrg44127/pdf/CHRG-110shrg44127.pdf

[11] Id.

[12] Bean, E. J. (2018).

[13] Tax haven banks and U.S. tax compliance: Hearings before the Permanent Subcommittee on Investigations of the U.S. Senate Committee on Homeland Security and Governmental Affairs. 110th Cong. (2008). https://www.govinfo.gov/content/pkg/CHRG-110shrg44127/pdf/CHRG-110shrg44127.pdf

[14] Bean, E.J. (2018).

[15] Hiring Incentives to Restore Employment Act, Pub. L. No. 111-147 124 Stat. 97 (2010). https://www.congress.gov/111/plaws/publ147/PLAW-111publ147.pdf

[16] Offshore tax evasion: the effort to collect unpaid taxes on billions in hidden offshore accounts: Hearings before the Permanent Subcommittee on Investigations of the U.S. Senate Committee on Homeland Security and Governmental Affairs. 113th Cong. (2014). https://www.govinfo.gov/content/pkg/CHRG-113shrg88276/pdf/CHRG-113shrg88276.pdf

[17] Bean, E. J. (2018).

[18] Bean, E. J. (2018).

[19] Offshore profit shifting and the U.S. tax code – part 2 (Apple Inc.): Hearings before the Permanent Subcommittee on Investigations of the U.S. Senate Committee on Homeland Security and Governmental Affairs. 113th Cong. (2013). https://www.govinfo.gov/content/pkg/CHRG-113shrg81657/pdf/CHRG-113shrg81657.pdf

[20] Offshore profit shifting and the U.S. tax code – part 2, p. 18 (2013).

[21] Offshore profit shifting and the U.S. tax code – part 2, p. 37 (2013).

[22] Bean, E.J. (2018).

[23] Bean, E.J. (2018).

[24] Caterpillar’s offshore tax strategy: Hearings before the Permanent Subcommittee on Investigations of the U.S. Senate Committee on Homeland Security and Governmental Affairs. 113th Cong. (2014). https://www.govinfo.gov/content/pkg/CHRG-113shrg89523/pdf/CHRG-113shrg89523.pdf

[25] Bean, E.J. (2018).

[26] Organization for Economic Cooperation. (2013). Action plan on base erosion and profit shifting. https://doi.org/10.1787/9789264202719-en

[27] Johnston, D. C. (2014, December 30). The legacy of Carl Levin. The American Prospect. https://prospect.org/power/legacy-carl-levin/

[28] “Inquiry into the Treatment of Detainees in U.S. Custody,” Senate Committee on Armed Services (Nov. 20, 2008), Conclusion 19 at xxix.

[29] “Inquiry into Counterfeit Electronic Parts in the Department of Defense Supply Chain,” Senate Committee on Armed Services (May 21, 2012), at i, vi.

[30] Section 818 of the 2012 National Defense Authorization Act, P.L. 112-81 (Dec. 31, 2011), https://www.congress.gov/bill/112th-congress/house-bill/1540.

[31] S. Doc. 113-34, at 14 (2014).

[32] S. Doc. 113-34, at 10 (2014).

[33] S. Doc. 113-34, at 19 (2014).

[34] Lesniewski, N., & Bowman, B. (2021, July 29). Former Sen. Carl Levin, champion of congressional oversight, dies at 87. Roll Call. https://rollcall.com/2021/07/29/former-sen-carl-levin-champion-of-congressional-oversight-dies-at-87/

[35] Neher, J., E. P. (Executive Producer). (2021, July 30). Remembering Carl Levin, Michigan’s titan of the U.S. Senate [Audio podcast episode]. In Detroit Today with Stephen Henderson. WDET. https://wdet.org/2021/07/30/remembering-carl-levin-michigans-titan-of-the-u-s-senate/